Component supply chain localisation crucial for UNLEASHING POTENTIAL

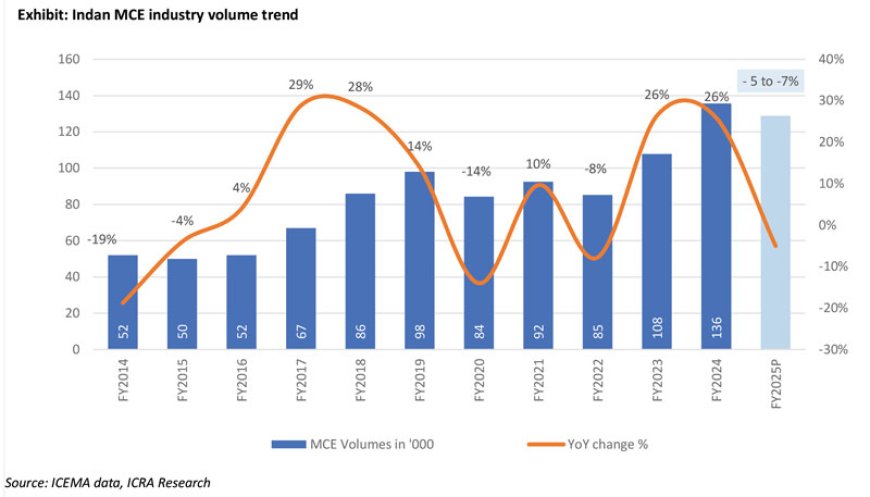

The Indian mining and construction equipment (MCE) industry has been witnessing a robust growth, crossing 1 lakh units in annual sale for the first time in history in FY2023 and setting yet another high with 1.36 lakh unit sales in FY2024. With a 12% compound annual growth rate in the last decade (FY2015 to FY2024), the industry surpassed Japan a few years ago to become the third largest MCE market globally (in terms of volumes sold) aspiring to become the second largest global market by 2030. Given the ambitious target of becoming a US$ 7 trillion economy by 2030, and multiplier effect of investments in infrastructure on GDP growth, the Government of India’s (GOI’s) policy focus on infrastructure development is expected to sustain. Furthermore, with the transition to the commercial equipment vehicle stage V (CEV-V) norms w.e.f. January 1, 2025, the Indian market is likely to come at par with prevalent European Union stage V (or Euro V) standards, which will help increase exports to more mature markets – like Europe and North America (as it would harmonise the production for domestic and export markets). Notwithstanding the transitory cyclicality (in sales), these favourable developments will drive the demand momentum for India’s MCE industry over the long term.

While the Indian MCE industry has an established manufacturing base, with over 50+ original equipment manufacturers (OEMs) operating in the country, the industry’s import dependence remains significant. As per ICRA’s estimates, India-based MCE OEMs, on an aggregate, import nearly 45-50% of their component requirement (by value) from the suppliers based out of China, Japan, South Korea and Germany among others, indicating significant headroom for domestic value addition. The high import dependence exposes the OEMs to fluctuations in forex and international freight costs, besides elongating their working capital cycle, because of the need to maintain higher inventory, thereby impacting their pricing competitiveness (for exports).

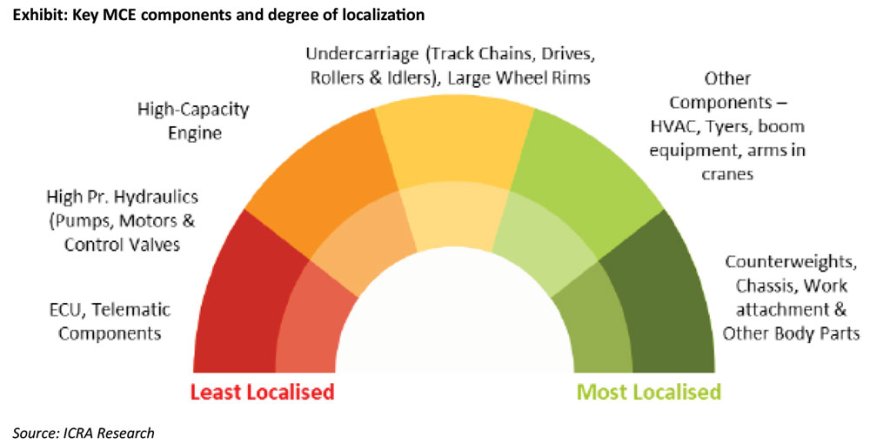

These indigenisation levels vary significantly across equipment categories (i.e. earthmoving, material handling, road construction, concrete equipment and material processing) – from >80% in back-hoe loaders to <20% in high tonnage/complex equipment like piling rigs. A few key component categories imported include - hydraulics, undercarriages and high-tech electronics like electronic control units (ECUs), sensors and telematics. These components are either technology-intensive parts or require large-scale manufacturing to attain economic viability. In addition, certain high tonnage fully built machinery and some steel alloy grades are also imported.

The key factor behind the high levels of imports so far has been the economic viability of setting up local manufacturing facilities (especially Tier-II/III component vendors) as visibility on critical volumes had been lacking due to insufficient domestic demand and limited exports (which, despite healthy growth, currently constitute only ~9-10% of overall sales volumes). One major reason for the same is the current emission regime, which excludes off-highway equipment, constituting 30-35% of overall sales volumes (unlike developed markets where there are common regulations). As domestic end-users are inclined to buy non-regulated CEVs (which end up being more economical in terms of cost of ownership), lack of regulations discourage investments and product development by local vendors. This impacts their global competitiveness. Additionally, unavailability of certain raw materials (select grades of steel alloys) and global procurement policies of multinational OEMs, also contribute to the import-dependent supply chains.

In recent years (and going forward), several factors have become favourable for increased localisation - including - increasing domestic demand, the PLI scheme for complementary sectors like specialty steel and auto components and China+1 strategies being adopted by multinational OEMs to diversify (or de-risk) their supply chains. The PLI schemes in other related sectors have been able to attract sizeable investments. While there is an overlap with the auto component industry, given the swifter shift to alternative fuel (mainly electric powertrains), a separate scheme for the MCE sector could help industry participants improve their export competitiveness. At a macro level, the GoI has been working towards improving the ease of doing business and creating a robust infrastructure to attract investment and improve the overall competitiveness of the domestic manufacturing industry.

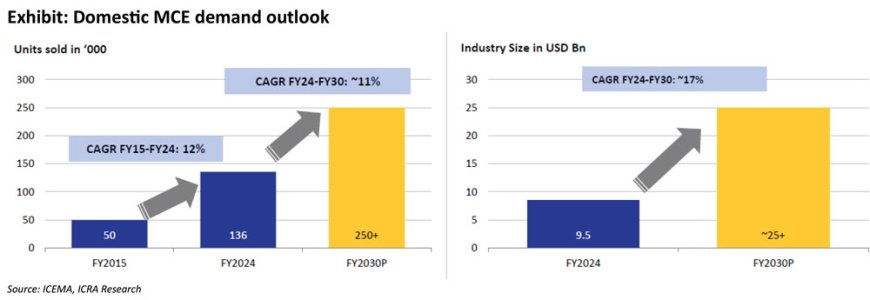

While certain components will continue to get imported, ICRA believes that the localised content could increase to over 70% in the next 5-7 years from ~50% at present. With a potential to become a Rs. 2.1 lakh crore market in annual revenues by FY2030, this increased localisation share would translate into incremental business opportunity of over Rs. 25,000 crore for the domestic MCE vendors. However, the focus towards increasing localisation must be consistent and with clear prioritisation.

ICRA opines that undercarriage components - like track chains, rollers and idlers etc - which provide a good market opportunity (given a large excavator market – domestic as well as global) are low on technological intensity and being heavy and logistically expensive to transport, these can be localised in the near term. Hydraulic components (motors, control valves etc.) could be the medium term (3–5-year horizon) target while electronic components (highly R&D intensive) could be a long-term option for local production.

Given the favourable demand scenario, improved localisation has become the need of the hour as it will help shield the supply chains of domestic manufacturers from geopolitical risks, improve operational efficiency, create more job opportunities and reduce carbon emissions (by reducing need for long-distance transportation). Improvement in cost competitiveness could also support increase in share of India’s exports from <2% in the long term. At present the domestic MCE vendors primarily rely on the OEMs to support their revenue, as the share of other business avenues like replacement demand and exports is relatively modest. With improvement in cost competitiveness, the export market would also provide significant growth opportunities to Indian component suppliers. With a strong supporting ecosystem of component manufacturers, the MCE OEMs will also thrive.

|

|

Ritu Goswami AVP and Sector Head, Corporate Ratings, ICRA |